The Financial Services AI Race:

A Decision Framework for the Institutions Still Deciding Which Side of the Gap They Will Be On

Published April 2026 | Arlo

Confidential -- Subscriber Use Only

EXECUTIVE SUMMARY

JPMorgan reported $2 billion in annual AI cost savings in its Q1 2026 earnings call. Goldman Sachs embedded AI across its "One GS 3.0" initiative. Morgan Stanley cut 2,500 jobs citing AI-driven efficiency. The Q1 2026 earnings season made one thing visible that had previously only been visible in analyst research: the AI gap in financial services is no longer theoretical. It is in the numbers.

This report is not about what JPMorgan is doing. It is about what the institutions that are not JPMorgan should be deciding right now -- and why the window to make that decision strategically, rather than reactively, is measurably shorter than most leadership teams believe.

The core finding: financial services AI advantage is compounding at the infrastructure layer, not the application layer. The institutions winning are not winning because they found better AI tools. They are winning because they built governance infrastructure, data architecture, and organizational capability before they scaled -- and that infrastructure is now the foundation for every new use case they deploy. The institutions in pilot mode are not one good tool away from catching up. They are three years of organizational learning behind, and the August 2, 2026 EU AI Act Phase Two deadline is about to make that gap legally material.

This report provides a decision framework for financial services leaders who need to assess their current position, identify the specific gaps that matter most, and make defensible resource allocation decisions before the regulatory deadline closes one degree of freedom they currently still have.

Estimated read time: 13 minutes.

THE CORE ARGUMENT

The financial services AI race is already over at the infrastructure layer. What remains is the application layer race -- and the institutions that built infrastructure first are winning that too, because governance-first deployment is faster deployment. Every institution not yet at production scale faces the same three decisions: how much of the JPMorgan gap is closeable, on what timeline, and at what cost. This framework helps answer all three.

THE EVIDENCE LAYER

What Q1 2026 earnings confirmed

JPMorgan's Q1 2026 earnings call was the first time a major financial institution publicly quantified its AI ROI at scale. The numbers: $2 billion in annual AI-driven cost savings, representing a 1:1 return on its $2 billion annual AI investment. CEO Jamie Dimon described the current results as "the tip of the iceberg," projecting deeper margin expansion by mid-2026. The efficiency ratio currently stands at 51%.

Goldman Sachs Q1 2026 highlighted AI as a growth accelerant embedded across the "One GS 3.0" initiative -- cloud migration, data infrastructure improvement, and firm-wide productivity. CEO David Solomon cited client demand for Goldman's AI implementation insights, positioning the bank as both an AI deployer and an AI thought leader for its clients.

Morgan Stanley cut approximately 2,500 jobs -- 3% of its workforce -- in March 2026, explicitly citing AI-driven efficiency. Its February 2026 survey of 935 executives found companies using AI for one or more years reported average net productivity gains of 11.5%.

What these three institutions share: all started building AI programs in 2022-2023. All built governance infrastructure before scaling. All are now extracting quantifiable returns. The institutions that started in 2025 or 2026 are not one year behind. They are behind by the organizational learning those programs represent.

The infrastructure gap -- what it actually means

McKinsey's 2026 analysis of banking AI identifies the competitive separation mechanism with precision. The institutions achieving 5%+ EBIT from AI share three structural characteristics: they built an AI Control Tower (central governance for risk guardrails, reusability, and value tracking), they invested in the full stack (engagement layer, decision layer, data/technology/operations foundation), and they led transformation at the business domain level rather than deploying AI as a technology overlay.

The institutions stuck in pilot mode share the opposite: fragmented governance with no clear ownership, legacy data architectures not built for AI inference, and AI initiatives led by technology teams without business domain redesign. McKinsey is specific: organizations with clear RAI accountability score 2.6 on governance maturity versus 1.8 without it. That gap compounds.

The competitive consequence McKinsey flags is stark: banking profit pools risk shrinking 9% globally if AI personalization is not deployed at scale -- with credit cards (34% at risk) and deposits (27% at risk) most exposed as consumers turn to third-party AI for financial guidance. The institutions that do not close the gap are not just leaving efficiency on the table. They are creating margin exposure that compounds as AI-native competitors and fintechs fill the gap.

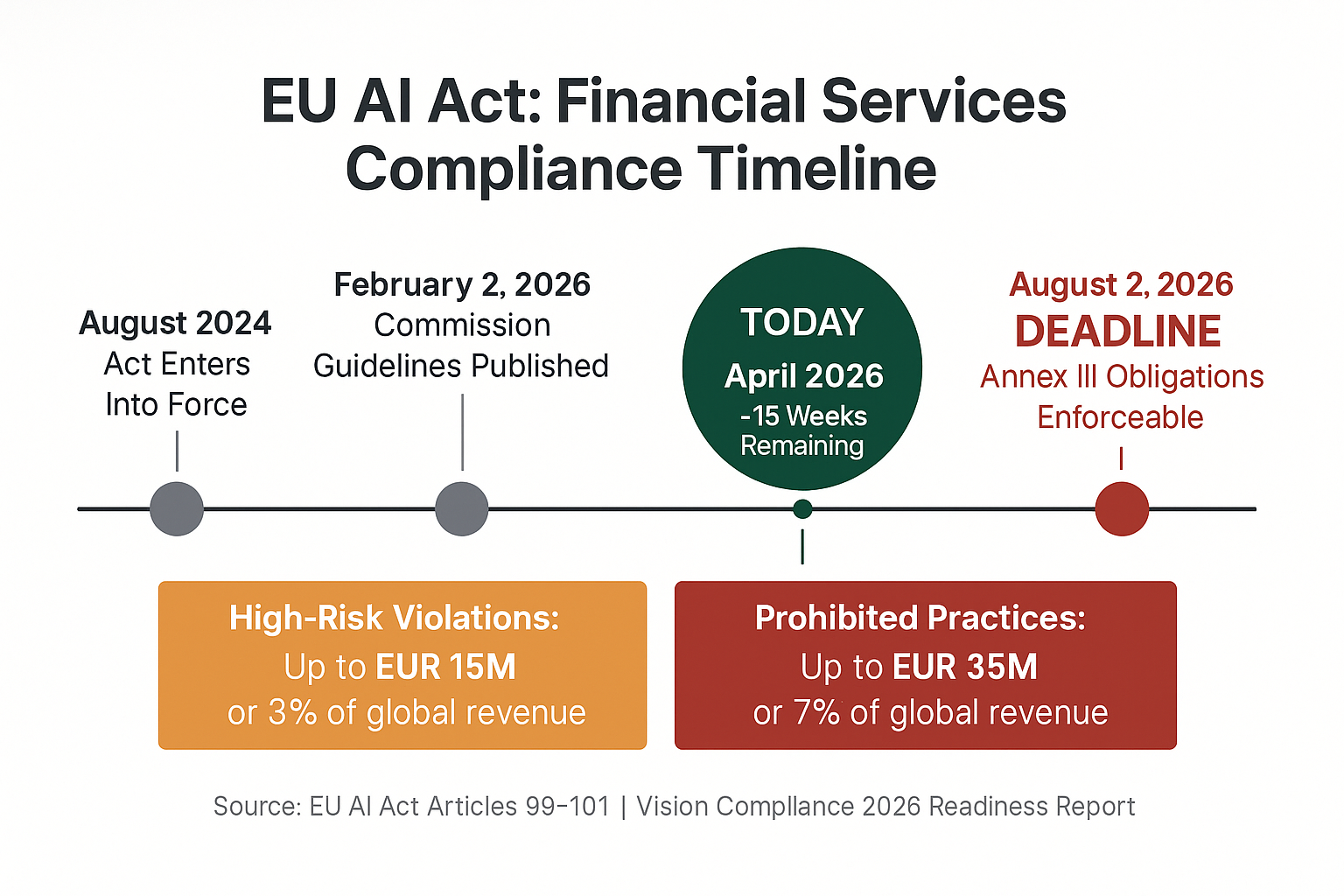

The EU AI Act as a forcing function -- what's actually required

The August 2, 2026 deadline is not a soft guideline. It is the date on which Annex III high-risk system obligations become enforceable for financial institutions operating in the EU. Here is what that means specifically for financial services:

Credit scoring and creditworthiness assessment are classified as high-risk AI under Annex III, Point 5(a). Most AI systems that evaluate individuals for access to credit -- including lending models, risk scoring, and loan origination AI -- fall under this classification. The obligations are specific and substantial:

- Risk management system (Article 9): A documented, lifecycle risk management framework specifically for the AI system -- not the institution's general risk framework applied retroactively.

- Data governance (Article 10): Relevant, representative, error-free datasets with documented bias mitigation processes.

- Technical documentation (Article 11): Full documentation of design, development, and validation -- accessible to regulators on request.

- Record-keeping (Article 12): Automatic logging for traceability, retained for a minimum of six months.

- Human oversight (Article 14): Trained staff with the ability to override, intervene, and suspend the system. An "off-switch" designed into the architecture, not added afterward.

- Conformity assessment (Article 43): Self-assessment for most Annex III systems; third-party notified body assessment for higher-risk applications.

The fine structure has two tiers: up to €15 million or 3% of global annual turnover for high-risk system violations; up to €35 million or 7% for prohibited practices. (Source: EU AI Act, Articles 99-101; Vision Compliance, 2026 EU AI Act Readiness Report confirms 78% of enterprises remain unprepared as of Q1 2026.)

The institutions that built governance infrastructure before scaling AI are already substantially compliant. Their credit scoring models have audit trails because the risk management function required them. Their human oversight frameworks exist because their compliance teams demanded them. Their technical documentation is current because legal was part of the deployment process. Compliance is a byproduct of how they built.

The institutions that are not compliant by August 2 face two simultaneous pressures: regulatory remediation consuming organizational bandwidth, and a compliance sprint that competes directly with new AI deployment capacity. The compliant institutions are using that same bandwidth to build the next use case.

The three use cases producing defensible ROI -- and why

The newsletter covered this at the broad level. The Intelligence Series goes deeper on the mechanism.

Fraud detection produces the clearest ROI in financial services AI because it has a binary counterfactual: fraud occurred or it did not. JPMorgan's $250M-$1B+ annual fraud savings is not an estimate of productivity improvement -- it is a documented reduction in fraud losses against a precisely quantifiable counterfactual. The ROI calculation requires no assumptions and no proxies. It survives any CFO review.

AML/KYC automation produces strong ROI through a different mechanism: compliance error costs are quantifiable because regulatory consequences are quantifiable. Fines, consent orders, remediation costs, and reputational damage all have dollar values. Reducing compliance errors and improving audit trail quality reduces the probability and magnitude of those outcomes. McKinsey documents 200-2,000% productivity gains in financial crime operations through agentic AI supervision of multiple sub-agents. That wide range reflects baseline variance across institutions -- the direction is consistent.

Credit underwriting efficiency produces ROI through operating leverage: faster decisions with the same or smaller credit team means more loan volume processed at lower unit cost. McKinsey documents 20-60% analyst productivity gains and 30% faster decisions. The value translates directly to revenue capacity.

The pattern across all three: they work because the counterfactual is measurable. Institutions deploying AI outside these three anchors -- in advisory, research synthesis, client communications -- are generating productivity gains they cannot yet translate to a defensible ROI case. That is not a reason to avoid those use cases. It is a reason to build the measurement infrastructure before deploying at scale.

THE DECISION FRAMEWORK

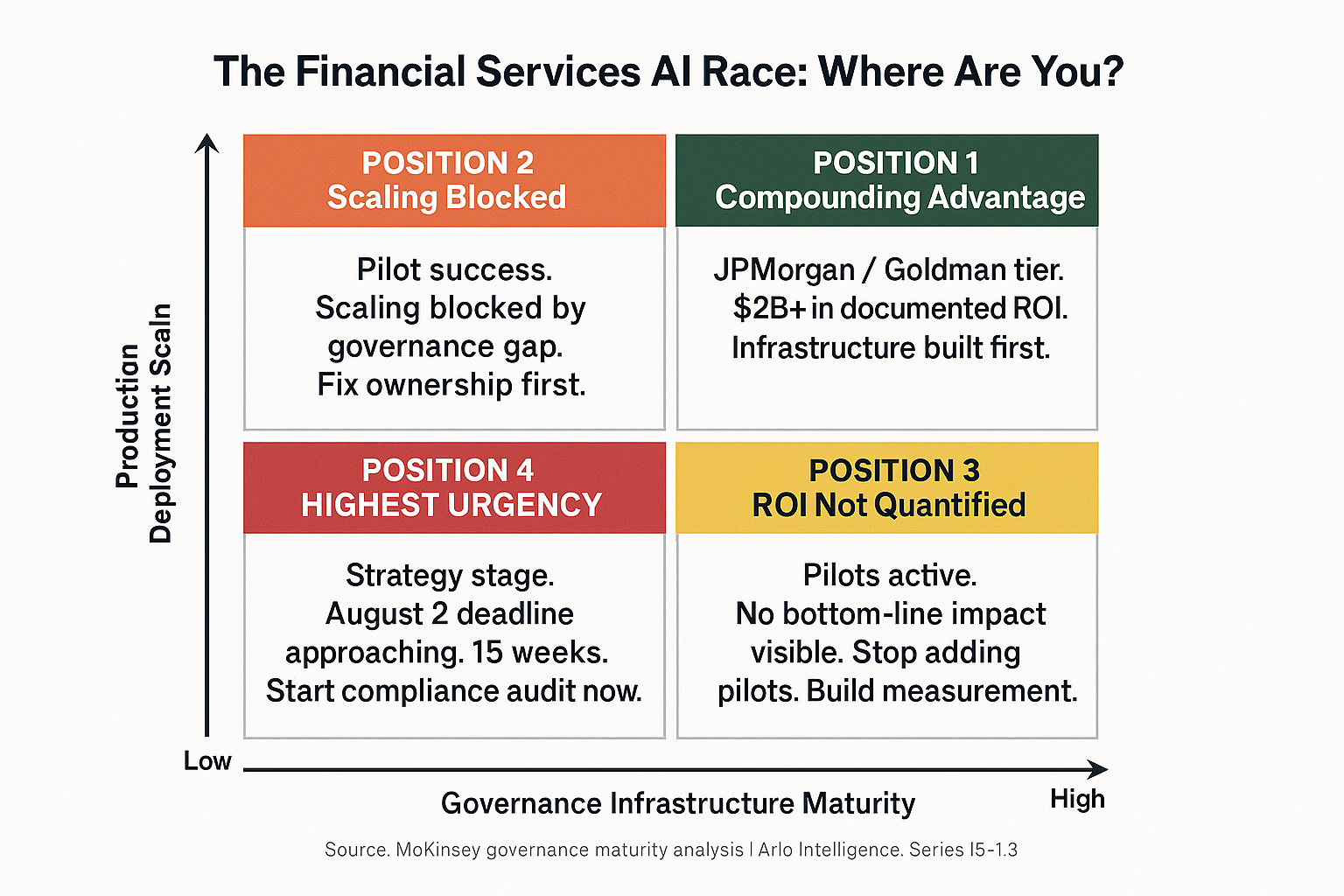

Every financial services leader reading this report is in one of four positions. The framework below helps identify which position and what the right decision is from each.

Position 1: Production at scale (JPMorgan/Goldman tier)

Characteristics: AI deployed in production across multiple functions, documented ROI, governance infrastructure in place, EU AI Act compliance largely embedded.

The decision: How to sustain the compounding advantage while managing the risks that scale creates. Primary focus: agentic AI governance, inference cost management at scale, talent retention for AI-fluent staff.

Position 2: Pilot success, scaling blocked

Characteristics: AI producing measurable results in pilots, scaling blocked by infrastructure gaps -- data architecture, governance, cross-functional team structure, or cost management.

The decision: Which blocking factor to address first. McKinsey's data is clear: governance ownership is the highest-leverage intervention. Organizations with clear RAI accountability score 44% higher on governance maturity. Fix accountability before investing in more technology.

Position 3: Pilots underway, ROI not quantified

Characteristics: Multiple AI initiatives active, no clear bottom-line impact visible, measurement infrastructure missing.

The decision: Stop adding pilots. Audit existing initiatives against the three proven ROI anchors (fraud, AML, credit underwriting). Identify whether productivity gains are measurable against a quantifiable counterfactual. Build measurement infrastructure before adding new use cases.

Position 4: Strategy stage, limited deployment

Characteristics: AI strategy documented, limited production deployment, EU AI Act compliance gap likely.

The decision: This is the highest-urgency position. August 2, 2026 is 15 weeks away. The compliance sprint required for high-risk system certification -- risk management documentation, technical files, human oversight frameworks, data governance -- requires six to twelve weeks of focused organizational effort minimum. Starting now is not comfortable. Starting in June is not viable.

The three questions that determine which decisions compound and which ones don't

1. Do we have clear ownership for AI governance, or is it distributed across functions without a single accountable leader? Organizations without clear RAI ownership are 44% lower on governance maturity and have materially longer time-to-production for every new use case.

2. For every AI system currently in production, can we produce the required EU AI Act documentation -- risk management framework, technical file, human oversight protocol, logging architecture -- within 30 days? If not, the gap between where you are and where the regulation requires you to be is measurable. Close it now, not in July.

3. What is the counterfactual for the AI productivity gains currently being measured in your organization? If the answer is "we can't quantify the counterfactual," the gains are real but not boardroom-defensible. Build the measurement framework before the next budget cycle.

THE PLAYBOOK

For the C-Suite (CEO / COO / CFO)

- Treat the EU AI Act deadline as a governance audit, not a compliance checkbox. The institutions that are already compliant built governance infrastructure as a precondition for scaling AI -- not as a response to a regulatory deadline. Running an AI Act compliance audit right now will tell you whether your AI program is built on a foundation that can scale, or whether it is built on a foundation that will require remediation every time you add a use case. That is a strategic insight, not just a legal one. Commission the audit now.

- Benchmark against JPMorgan's trajectory, not your peer group. Most financial institution AI benchmarking compares against direct competitors. JPMorgan's program is three years into production scale, has $2 billion in documented annual value, and is targeting 1,000 production use cases by end-2026. Understanding the specific gap -- in use case deployment, governance infrastructure, data architecture, and organizational capability -- is the first step to building a program that closes it. Your peer group's performance is the floor, not the target.

- Require a quantifiable counterfactual for every AI initiative before approving production scale. The difference between JPMorgan's $2 billion in documented savings and a competitor's "significant productivity improvements" is not the quality of the AI. It is the measurement framework. Before any AI program scales to production, require the team to answer: what is the dollar value of the outcome we are trying to influence, and what is the baseline without AI? If they cannot answer, the program is not ready to scale.

For CMOs and Marketing VPs in Financial Services

- Map every AI marketing application against the EU AI Act high-risk classification criteria before the next campaign. Credit-related marketing, personalization for financial product targeting, and AI-driven customer scoring may trigger Annex III high-risk classification under Point 5(a) -- particularly if the AI is evaluating individuals' creditworthiness as part of the targeting logic. Verify with legal before the deadline. The fine for a non-compliant marketing AI is the same as for a non-compliant credit scoring model.

- The JPMorgan wealth management results (83% faster research, 3.4x advisor productivity) represent a direct competitive threat to client acquisition and retention in your market. If your advisory teams are not generating client insights at comparable speed, they are competing at a structural disadvantage against institutions that are. The question for your function is not whether AI-augmented advisory is possible -- it is confirmed and documented. The question is when your institution will close that gap and what the cost of delay is in client attrition.

For Chief Risk Officers and Chief Compliance Officers

- Run the EU AI Act readiness audit now -- specifically Articles 9, 10, 11, 12, 14, and 43 -- for every credit scoring and creditworthiness AI system in production. The EBA's 2025 guidance confirms that existing banking frameworks (CRD/CRR, DORA) partially satisfy some AI Act requirements, but the AI Act adds obligations that existing risk management frameworks do not address -- particularly around fundamental rights impact assessment, automatic logging, and conformity assessment documentation. The partial overlap is not full compliance. Identify the gaps explicitly by May 15 to have time to close them before August 2.

- Treat the conformity assessment process as a governance infrastructure investment, not a one-time compliance event. Organizations that build conformity assessment capability in-house -- the documentation templates, the assessment processes, the cross-functional review structures -- will deploy new AI use cases faster than organizations that rely on external consultants for each new system. Every system that goes through conformity assessment for the August deadline is also the template for every system deployed afterward.

DATA HIGHLIGHTS

SOURCES

McKinsey, "Extracting Value from AI in Banking: Rewiring the Enterprise" (2026)

McKinsey, "How Financial Institutions Can Improve Their Governance of Gen AI" (2026)

McKinsey, State of AI Trust in 2026 -- Shifting to the Agentic Era

JPMorgan Chase, Q1 2026 Earnings Call (April 14, 2026) -- CNBC, Investing.com coverage

Goldman Sachs, Q1 2026 Earnings Results (April 13, 2026) -- Goldman Sachs press release

Morgan Stanley, AI Adoption Survey (February 2026, 935 executives, US/Germany/Japan/Australia)

EU AI Act, Regulation (EU) 2024/1689 -- Articles 9-15, 43, 49, 72, 99-101

European Banking Authority, "AI Act Implications for the EU Banking Sector" (November 2025)

Vision Compliance, 2026 EU AI Act Readiness Report -- 78% of enterprises unprepared figure

EBA supervisory convergence guidance, 2025-2026

Produced with AI assistance and human editorial review.

Arlo Intelligence Series | Confidential -- Subscriber Use Only | April 2026 | Page [X] of [X]